Introduction

India's fintech sector operates under a layered regulatory framework that has undergone a fundamental transformation. The Reserve Bank of India's Master Directions now serve as the authoritative, consolidated rulebook—replacing thousands of scattered circulars that previously made compliance chaotic and prone to gaps.

Fintechs face a structurally different compliance burden than traditional banks. Unlike traditional banks, fintechs often wear multiple regulatory hats simultaneously—operating as digital lenders, payment aggregators, PPI issuers, and Lending Service Providers. This means multiple Master Directions may apply at once, raising compliance stakes significantly.

This guide covers which Master Directions apply to fintechs, what obligations they impose, and how to build a defensible compliance posture. The 2024-2025 update cycle tightened requirements across digital lending, payment aggregation, and mobile security—so the details below reflect what's actually enforceable today.

TLDR:

- RBI replaced 9,445 circulars with 244 unified Master Directions in November 2025

- Digital lending fintechs must enforce strict 1-day cooling-off periods and direct fund flows

- Payment aggregators must meet ₹15-25 crore net worth thresholds and maintain strict escrow controls

- RBI now mandates RASP, code obfuscation, and device binding for mobile app security

- Cyber incidents must be reported to RBI within 2-6 hours of detection

- Full-KYC PPI wallets can now link with third-party UPI apps under December 2024 amendments

What are RBI Master Directions and why do they matter for fintechs

RBI Master Directions are consolidated regulatory instructions that bring together all applicable circulars, notifications, and guidelines for a specific entity type or activity into a single, continuously updated document. This consolidation eliminates the need to trace hundreds of older circulars to determine what still applies.

In November 2025, the RBI completed a landmark regulatory reorganization, issuing 244 Master Directions across 11 types of regulated entities while simultaneously withdrawing 9,445 obsolete circulars. For fintechs, this means relying on legacy circulars is now legally invalid—compliance teams must map internal policies exclusively to the new Master Directions.

Legal standing and enforcement authority

Master Directions carry binding regulatory force, issued under robust statutory powers:

- Section 35A read with Section 56 of the Banking Regulation Act, 1949

- Section 45L of the Reserve Bank of India Act, 1934

- Section 18 read with Section 10(2) of the Payment and Settlement Systems Act, 2007

Non-compliance can result in monetary penalties (running into crores of rupees), license revocation, or regulatory action. The RBI's 2024-25 enforcement data shows 79 enforcement actions totaling ₹32.91 crore, with NBFCs accounting for 61% of all penalty cases.

Who is bound by Master Directions?

Coverage depends on how your business is classified under RBI's framework:

- Regulated Entities (REs) — banks and NBFCs are directly bound by Master Directions

- Licensed fintechs — Lending Service Providers, Payment Aggregators, and PPI issuers are covered through Master Directions specific to their licensed activity

- Unlicensed technology providers — outside direct scope, but RE partners will contractually push compliance obligations downstream, making this a practical requirement even for pure tech vendors

Key RBI Master Directions fintechs must know

The applicable set of Master Directions depends on a fintech's business model. Here's a categorized map of the most relevant frameworks:

Payments and aggregator fintechs

Payment Aggregator Master Direction (September 2025)

The Master Direction on Regulation of Payment Aggregators, issued September 15, 2025, supersedes the original 2020 guidelines. This is the primary regulatory framework for payment fintechs.

Key requirements:

- Maintain net worth of ₹15 crore at application, scaling to ₹25 crore by the end of the third financial year

- Hold escrow accounts with strict restrictions on permissible debits

- Complete merchant onboarding due diligence and run ongoing monitoring

- Settle funds to merchants on T+1 timelines unless contractually agreed otherwise

Any non-bank entity handling funds qualifies as a Payment Aggregator and must be RBI-authorized. Enforcement is active: Cashfree Payments was penalized ₹3.1 lakh in March 2026 for impermissible escrow account debits.

Prepaid Payment Instruments Master Direction (Updated February 2024)

The Master Direction on PPIs, initially issued August 2021, governs wallet and prepaid card fintechs.

Critical provisions:

- Distinguish Full-KYC and minimum-KYC PPI categories, each carrying separate transaction limits

- Meet interoperability requirements that enable cross-wallet transactions

- Implement the December 2024 amendment permitting full-KYC PPI holders to link wallets with third-party UPI apps

This amendment breaks the closed-loop nature of PPIs, requiring infrastructure upgrades to enable wallet discovery on major UPI platforms.

Digital lending fintechs and NBFCs

Digital Lending Directions (2025)

The RBI Digital Lending Directions, 2025 apply to all entities offering loans via digital platforms—whether banks, NBFCs, or through Lending Service Providers.

Core mandates:

- Provide a Key Fact Statement (KFS) to borrowers before disbursal

- Calculate APR on an all-inclusive basis, covering processing fees and other charges

- Route funds directly to borrowers — no LSP intermediation permitted

- Comply with LSP conduct standards and data privacy restrictions

- Register all Digital Lending Apps on RBI's CIMS portal

NBFC Scale-Based Regulation Framework

For NBFCs operating digital lending platforms, the Master Direction on NBFC Scale-Based Regulation, issued October 2023, adds a second compliance layer. It categorizes NBFCs into four tiers by size and risk: Base Layer (NBFC-BL), Middle Layer (NBFC-ML), Upper Layer (NBFC-UL), and Top Layer (NBFC-TL).

Fintech NBFCs with assets below ₹1,000 crore are classified as Base Layer entities. This framework sets requirements for:

- Capital adequacy requirements

- Board governance responsibilities

- IT governance standards

- KYC and outsourcing risk controls

Digital lending compliance: what fintechs must get right

Key fact statement and APR disclosure

The KFS requirement mandates disclosure of all charges, Annual Percentage Rate (APR), loan terms, cooling-off period rights, and recovery agent details before loan disbursal.

APR calculation must include:

- Processing fees

- Insurance charges linked to the loan

- Verification charges

- Maintenance charges

For floating rate loans, revised APR must be communicated via SMS/email each time rates change.

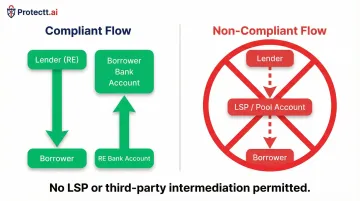

Fund flow restrictions

The RBI maintains zero tolerance for LSPs acting as financial intermediaries. Digital Lending Guidelines explicitly state: "REs shall ensure that all loan servicing, repayment, etc., shall be executed by the borrower directly in the RE's bank account without any pass-through account/pool account of any third party."

Fund flow rules require that:

- Loan disbursals must go directly to borrower's bank account

- Repayments must flow directly to RE's account

- No LSP or third-party intermediation permitted

- Payment Aggregators performing LSP functions are subject to both PA and Digital Lending regulations

Data privacy obligations for LSPs

LSPs cannot store customers' personal data beyond basic operational minimums. The guidelines prohibit: "REs shall ensure that no biometric data is stored/collected in the systems associated with the DLA of REs/their LSPs, unless allowed under extant statutory guidelines."

| Data Type | Permitted |

|---|---|

| Name, address, contact details | ✓ Yes |

| Operational data for service delivery | ✓ Yes |

| Biometric data (without statutory approval) | ✗ No |

| Excessive personal information beyond operational needs | ✗ No |

Cooling-off period and grievance redressal

The 2025 Directions reduced the cooling-off period to 1 day for all loans regardless of tenor. During this period, borrowers can exit without penalty, though a reasonable one-time processing fee can be retained.

Grievance redressal requirements:

- LSPs with direct borrower interface must appoint a nodal Grievance Redressal Officer

- REs remain ultimately responsible for resolving complaints arising from LSP actions

- Unresolved complaints escalate to the RBI's Integrated Ombudsman Scheme

First Loss Default Guarantee (FLDG) framework

The Guidelines on Default Loss Guarantee, issued June 2023 and restored for NBFCs in February 2026, permit structured risk-sharing arrangements.

Key provisions:

- Maximum 5% coverage cap on outstanding portfolio

- Must be invoked within 120 days of overdue

- Backed by cash deposits, Fixed Deposits with lien, or Bank Guarantees

- Full disclosure required in loan agreements

IT governance, cybersecurity, and mobile app security requirements

Digital payment security controls (2021)

The Master Direction on Digital Payment Security Controls, issued February 2021, applies to banks, Small Finance Banks, Payments Banks, and credit-card issuing NBFCs.

Mobile app security mandates:

- Device binding — apps must implement binding mechanisms to tie sessions to verified devices

- Code obfuscation to prevent reverse engineering and tampering

- Version control — older app versions must be deactivated within six months

- Secure storage — no sensitive data in HTML hidden fields or client-side storage

While this direction directly binds REs, fintechs building apps for regulated entities must ensure their technology meets these standards contractually—making mobile app security compliance a practical requirement for tech vendors.

Protectt.ai's RASP platform maps directly to these mandates — covering anti-tampering, code obfuscation, Zero Trust Device & SIM Binding, and real-time threat detection, all with zero performance overhead. For fintech NBFCs deploying mobile lending or payment apps, these controls can be embedded at the SDK level without slowing app performance.

Outsourcing of IT services (April 2023)

The Master Direction on Outsourcing of IT Services, issued April 2023, governs fintech technology vendors serving REs.

Critical requirements:

- Audit rights: Contracts must grant REs and RBI authority to inspect service providers

- Data localization: All data must be stored in India per regulatory requirements

- Business continuity: Service providers must maintain documented BCP/DR plans

- Core function restrictions: REs cannot outsource core decision-making (credit appraisal, KYC) to unregulated entities

These aren't theoretical requirements. The RBI cancelled Certificates of Registration for both Zavron Finance and X10 Financial Services over outsourcing violations — a clear signal that non-compliance carries existential consequences for regulated entities and their vendors alike.

Cyber incident reporting requirements

The RBI maintains an extremely tight reporting window for cyber breaches. Security Incident Reporting requirements mandate notification to RBI within 2 to 6 hours of incident detection.

This leaves no room for delayed forensic investigations. CTOs and CISOs must deploy automated threat detection that can surface and classify incidents fast enough to meet that window — manual investigation processes simply won't hold up.

The FREE-AI framework (December 2024)

Beyond reactive breach reporting, the RBI is also shaping how AI itself gets governed. On December 26, 2024, the RBI announced the Framework for Responsible and Ethical Enablement of Artificial Intelligence (FREE-AI) in the Financial Sector.

Scope: Banks, NBFCs, FinTechs, and Payment System Operators using AI/ML in credit scoring, fraud detection, or customer onboarding.

Expected requirements:

- Documented risk assessment for AI models

- Bias evaluation and mitigation frameworks

- Explainability standards for AI-driven financial decisions

Fintechs should begin preparing AI governance documentation now, ahead of formal framework issuance.

KYC, AML, and consumer protection compliance

Master Direction on KYC (2016) and 2024 Amendments

The Master Direction on KYC, originally issued 2016, received a critical update in November 2024 enabling Customer Due Diligence at the Unique Customer Identification Code (UCIC) level.

Key provision: If an existing KYC-compliant customer desires to open another account or avail any other product from the same RE, there shall be no need for a fresh CDD exercise as far as identification is concerned.

This reduces onboarding friction and enables cross-selling across products. Product teams should redesign user flows to take advantage of this provision.

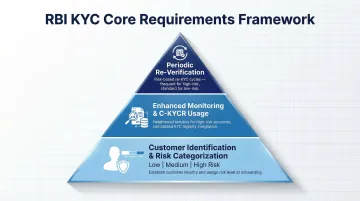

Core KYC requirements:

- Customer identification and risk-based categorization (low/medium/high)

- Enhanced monitoring for high-risk accounts

- Required use of Central KYC Records Registry (C-KYCR)

- Periodic re-verification based on risk category

AML/CFT obligations

Under the Prevention of Money Laundering Act (PMLA) as operationalized through RBI's KYC Directions:

- Deploy automated systems to detect and flag suspicious transaction patterns

- Report suspicious transactions to FIU-IND without exception

- Retain records for a minimum of 5 years after the business relationship ends

- Train all relevant staff on AML/CFT obligations regularly

For fintechs dealing in virtual digital assets, registration with FIU-IND and AML compliance is mandatory under the March 2023 PMLA amendment.

Consumer protection and grievance redressal

Consumer protection requirements are embedded across multiple Master Directions:

- Fair practices codes for lending and recovery

- Prohibition of unfair loan recovery practices

- Mandatory grievance redressal mechanisms

- Transparency in charges and terms

- RBI's Integrated Ombudsman Scheme as escalation path

The Reserve Bank Integrated Ombudsman Scheme, 2021 covers all commercial banks, NBFCs with assets of ₹100 crore and above, and System Participants (including non-bank PPI issuers).

RBI enforcement actions in this space most often stem from gaps in grievance redressal and opaque fee disclosures — areas where fintechs should prioritize internal audits.

Building a practical compliance framework for fintechs

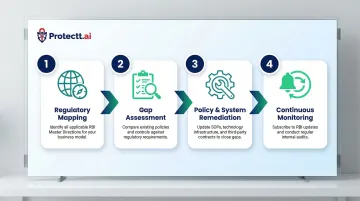

Four-step compliance approach

1. Regulatory Mapping

Identify which Master Directions apply based on your licensed activities and partnerships:

- Payment Aggregator? → PA Master Direction

- Digital lender or LSP? → Digital Lending Directions

- PPI issuer? → PPI Master Direction

- Fintech NBFC? → NBFC Scale-Based Regulation + IT Governance + KYC + Outsourcing

2. Gap Assessment

Compare current policies, controls, and systems against each applicable Master Direction:

- Document existing controls

- Identify gaps in policy, process, or technology

- Prioritize gaps by regulatory risk and enforcement likelihood

3. Policy and System Remediation

Update internal SOPs, technology configurations, and contractual arrangements:

- Revise lending agreements to include mandatory KFS and APR disclosures

- Configure fund flows to eliminate LSP intermediation

- Implement mobile app security controls (RASP, code obfuscation, device binding)

- Update vendor contracts to include audit rights and data localization clauses

4. Continuous Monitoring

Set up alerts for Master Direction amendments and schedule periodic internal audits:

- Subscribe to RBI notifications

- Review the RBI Master Directions page quarterly

- Maintain a regulatory change management process

- Conduct internal audits semi-annually

Technology in compliance automation

Fintechs can now map specific regulatory requirements directly to system-level controls:

- Encode KYC timelines into onboarding workflows

- Automate APR disclosures in KFS generation

- Embed security controls into mobile app SDKs

The cost of getting this wrong is concrete. In FY 2024-25, the RBI levied penalties totaling ₹32.91 crore across 79 enforcement actions. High-profile cases include:

- Innofin Solutions (LenDenClub): ₹1.99 crore for unauthorized fund routing

- NDX P2P (LiquiLoans): ₹1.92 crore for LSP fund flow violations

Both violations were operational, not strategic — the kind that automated controls and clear fund flow configurations are specifically designed to prevent.

Board-level compliance ownership

Enforcement risk doesn't stop at the operations team. Master Directions now explicitly assign governance responsibilities to boards and senior management.

Required governance structures:

- Board-approved IT/cybersecurity policy

- Compliance function with clear reporting lines to board

- Documented evidence of periodic reviews

- Incident response plans with board escalation protocols

All of these are subject to RBI inspection. Platforms like Protectt.ai reduce manual preparation burden by providing pre-mapped security controls with automated audit trails and structured reporting — cutting audit preparation from weeks to hours.

Frequently asked questions

What are RBI Master Directions, and how are they different from circulars?

Master Directions are consolidated, continuously updated regulatory documents that replace hundreds of individual circulars on a specific topic or entity type. They offer a single authoritative reference, eliminating the need to verify whether older circulars still apply.

Which RBI Master Directions apply specifically to fintech companies?

Applicable Master Directions depend on the fintech's activity: Payment Aggregator Guidelines for PA fintechs, Digital Lending Guidelines for lending platforms/LSPs, PPI Master Directions for wallet issuers, and NBFC Master Directions (Prudential Norms, IT Governance, KYC, Outsourcing) for fintech NBFCs. Many fintechs are subject to multiple simultaneously.

What are the penalties for non-compliance with RBI Master Directions?

Penalties range from monetary fines (which can run into crores of rupees) to suspension or cancellation of license/authorization. Recent RBI enforcement actions indicate a rising trend in both the frequency and severity of penalties for compliance lapses, with reputational damage as an additional consequence.

Does the Master Direction on Digital Payment Security Controls apply to fintech apps?

The direction directly binds banks and credit-card issuing NBFCs. However, fintechs building apps for these regulated entities must meet the same security standards through contractual obligations, making mobile app security compliance a practical requirement for fintech technology vendors.

How often are RBI Master Directions updated, and how should fintechs track changes?

Master Directions are updated on a rolling basis — the KYC Directions were amended in November 2024 and PPI Master Directions in December 2024. Fintechs should subscribe to RBI notifications and review the Master Directions page regularly to catch changes as they occur.

What is the difference between a Regulated Entity (RE) and a Lending Service Provider (LSP) under RBI's Digital Lending framework?

REs (banks, NBFCs) are directly licensed and fully accountable to the RBI for all lending activities. LSPs are technology agents performing lending functions on behalf of REs — they are not directly licensed but must operate within the guardrails set by Digital Lending Guidelines, with REs remaining ultimately responsible for LSP conduct.