What is OWASP MASVS and why does it matter for BFSI mobile apps?

OWASP MASVS (Mobile Application Security Verification Standard) is the industry benchmark for mobile app security. For BFSI institutions, it matters because it provides a structured, risk-tiered framework (L1, L2, and Resilience) that maps directly to regulatory expectations from bodies like RBI, SEBI, and PCI DSS—helping banks, insurers, and fintechs systematically identify and remediate mobile security vulnerabilities before they lead to breaches or regulatory penalties.

Which OWASP MASVS levels are applicable to banking and financial apps?

BFSI mobile apps typically require MASVS-L2 (Defense-in-Depth) as a baseline, which mandates secure data storage, strong cryptography, and network security controls. High-value transaction apps also require MASVS-R (Resilience), which covers reverse engineering resistance and anti-tampering controls. Protectt.ai assesses your specific regulatory context—RBI, NPCI, SEBI, or PCI DSS—to recommend and validate the precise MASVS levels applicable to your application.

How does OWASP MASVS testing help with RBI Digital Payment Security Controls compliance?

RBI's Digital Payment Security Controls mandate robust mobile application security, including protection against app tampering, secure authentication, and encrypted data transmission. OWASP MASVS testing validates all these controls systematically. Protectt.ai's AppProtectt platform provides 100+ RASP-based security features that directly fulfill RBI requirements, and our testing reports are structured to serve as compliance evidence during regulatory audits.

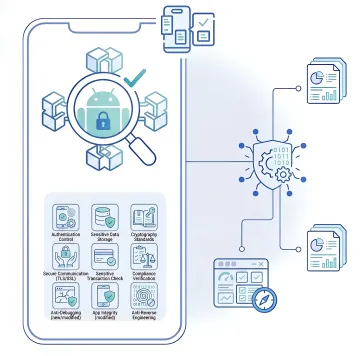

What does the OWASP MASVS mobile security testing process involve?

The process includes five structured phases: regulatory scoping and MASVS level mapping, static analysis (SAST) of source code and binaries, dynamic analysis (DAST) of live app sessions, runtime and behavioral attack simulation using RASP tooling, and a detailed compliance gap report with remediation guidance. A re-test and compliance attestation are provided after vulnerabilities are addressed.

How long does an OWASP MASVS assessment take for a BFSI mobile app?

A standard OWASP MASVS L1/L2 assessment for a BFSI mobile app typically takes 2–4 weeks, depending on app complexity, number of features, and platform coverage (Android, iOS, or both). The Resilience (MASVS-R) assessment, which includes runtime attack simulation and anti-tamper testing, may require an additional 1–2 weeks. Protectt.ai provides a scoping call to give you a precise timeline before engagement begins.

What types of vulnerabilities does OWASP MASVS testing uncover in financial apps?

MASVS testing identifies insecure local data storage exposing sensitive financial data, weak cryptographic implementations, improper session management, missing certificate pinning enabling MITM attacks, insufficient binary protections allowing reverse engineering, hardcoded credentials, and insecure inter-process communication. For BFSI apps, these vulnerabilities can directly lead to account takeovers, transaction fraud, and regulatory non-compliance.

Does Protectt.ai provide remediation support after identifying MASVS gaps?

Yes. Protectt.ai provides detailed, risk-prioritized remediation guidance for every finding, including code-level recommendations and SDK-based fixes. Our AppProtectt and CodeProtectt solutions can directly address many MASVS control gaps—such as runtime protection, code obfuscation, and secure device binding—without requiring significant in-house development effort. We also conduct a formal re-test to validate that all remediated issues are resolved before issuing the compliance attestation.

Is Protectt.ai's MASVS testing relevant for insurance and NBFC mobile apps, not just banks?

Absolutely. OWASP MASVS compliance is equally critical for insurers, NBFCs, fintechs, and payment aggregators. Protectt.ai's platform is purpose-built for the entire BFSI spectrum and trusted by organizations such as ICICI Lombard, LIC, Bajaj Finserv, Shriram Finance, and multiple NBFCs. Our MASVS assessments account for sector-specific regulatory requirements beyond core banking, including IRDAI guidelines and RBI NBFC directions.